Digital Dives

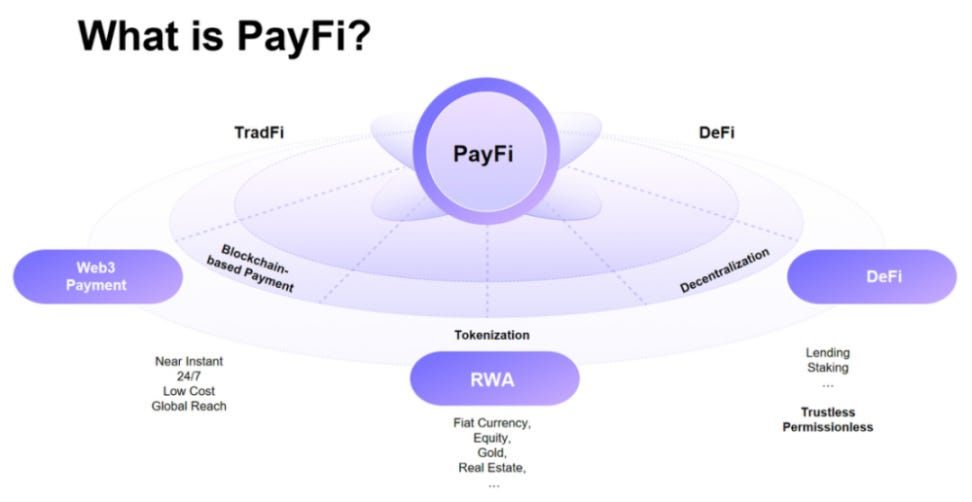

A defining feature of the financial world is its ability to evolve. From the barter systems of ancient civilizations to the digital transactions that power our modern economy, the mechanisms through which we exchange value have continuously transformed. Among the latest innovations worth watching is PayFi—a pragmatic approach to payments that combines the efficiency of blockchain technology with the reliability of traditional financial infrastructure.

I’ll be honest, I don’t love the name, but PayFi, short for Payment Finance, represents the convergence of traditional payment infrastructure with blockchain technology and decentralized finance (DeFi) protocols. Unlike many crypto innovations that tried to position themselves as replacements for existing systems, PayFi takes a more pragmatic approach—enhancing rather than eliminating traditional payment rails.

At its core, PayFi addresses three persistent pain points in our current payment ecosystem:

What makes PayFi particularly interesting is its hybrid nature. Rather than forcing users to choose between traditional finance and crypto, it creates bridges between these worlds, allowing value to flow seamlessly across previously siloed systems.

Several key technologies support the growth of the PayFi ecosystem. Companies like BoomFi help bridge the gap between crypto and traditional payments by offering tools that connect blockchains to everyday financial systems. Their services include support for accepting crypto payments, managing digital wallets, settling transactions in stablecoins, and converting between crypto and fiat currencies.

By making these tools easy to use—whether through simple interfaces or developer-friendly integrations—BoomFi and others help traditional fintechs and payment providers adopt crypto-powered features without needing deep blockchain expertise. However, it’s not just startups driving this evolution. Payment giants like Visa and Mastercard are actively building in this space as well, integrating blockchain-based infrastructure into their global networks. Such infrastructure is critical to translating PayFi’s potential into practical, everyday financial experiences.

High-throughput blockchain networks like Solana, Ethereum Layer 2s, and others provide the infrastructure for instant, affordable payments, processing thousands of transactions per second at costs below $0.01. Stablecoins pegged to fiat currencies eliminate volatility concerns while maintaining the programmability and efficiency of blockchain technology. Smart contracts enable complex payment flows that would be difficult or impossible in traditional systems, such as automatic invoice splitting, conditional payments, or recurring crypto payments. Finally, tokenized real-world assets (RWAs) represent traditional financial assets on-chain, unlocking new liquidity and financing options for businesses and individuals.

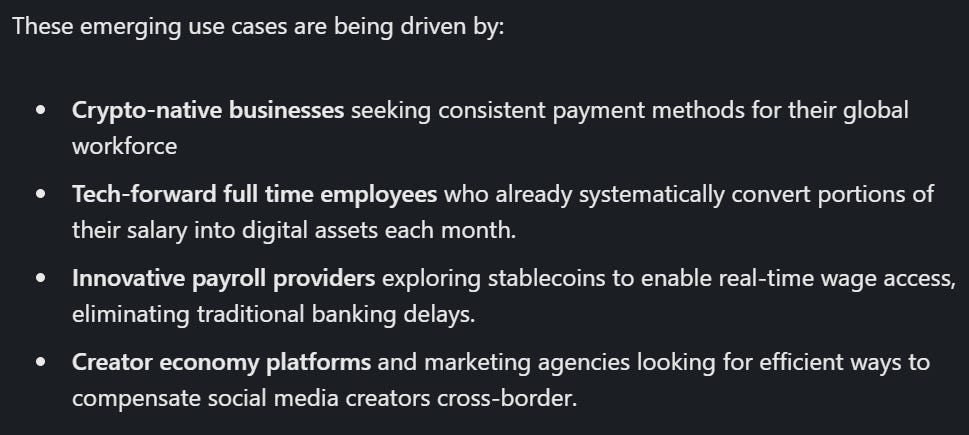

Though still early, PayFi is already showing real-world traction across a range of financial use cases.

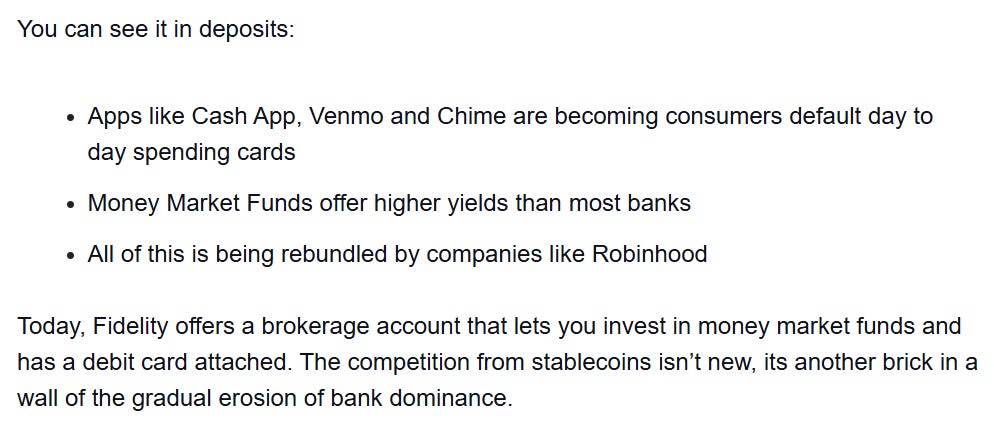

PayFi's rise reflects a broader shift in how we think about financial services. Traditional banks, neobanks, and now DeFi-native platforms each offer distinct models with different trade-offs.

What sets DeFi banks apart is their architecture. Instead of holding user assets, they typically operate on self-custody principles—reducing counterparty risk and preventing rehypothecation. This empowers users, but also places more responsibility on them, including key management and exposure to smart contract vulnerabilities with limited recourse. Transparency is another hallmark: reserves and transactions are visible on-chain, offering a level of visibility rarely found in traditional systems—though often at the expense of privacy.

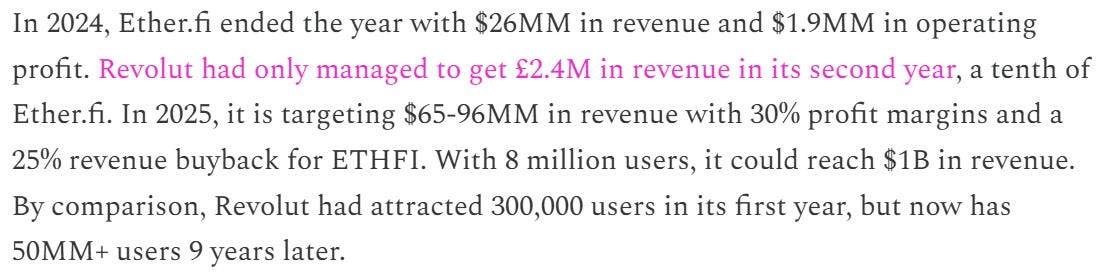

These platforms are also structurally lean. Many operate with teams of just 25–50 people, yet manage institutional asset volumes. While this staffing advantage may shrink as regulatory demands grow, the underlying operational efficiencies remain significant.

Those efficiencies translate to tangible user benefits. While traditional neobanks might offer 0.4–1.2% cashback on purchases, PayFi-powered cards can offer up to 3%, enabled by lower infrastructure costs and yield-driven incentives. Leaner teams also allow these platforms to invest more aggressively in growth. The economics are striking: some DeFi protocols reach profitability in under two years—a stark contrast to the decade-long ramp many neobanks faced. With comparable customer lifetime values ($500–$1,000) and stronger margins, PayFi-native banking models offer a credible path to sustainable, scalable growth—if they can keep pace with regulation and manage their unique risks.

For established financial institutions, PayFi presents both disruption and opportunity. While it may challenge legacy models—particularly in areas like cross-border payments and custody—it also unlocks new efficiencies, revenue streams, and innovations for those ready to evolve.

Forward-thinking banks and payment processors are already exploring how to embed these principles into their existing operations, building on trusted brands and customer relationships rather than competing head-on with crypto-native challengers. In fact, gradual integration may be a strategic advantage: by layering PayFi capabilities onto familiar interfaces, incumbents can deliver blockchain benefits without imposing the learning curve or perceived risk of newer platforms.

Some PayFi concepts are also taking shape outside of blockchain environments, creating new competitive arenas in more traditional fintech spaces.

Key areas of exploration include:

By adopting PayFi as a toolkit rather than a competitor, incumbents can preserve their core advantages—brand trust, scale, and customer base—while enhancing their infrastructure for the online age.

At Aquanow, we work with institutions to integrate digital asset capabilities into their existing infrastructure—helping them stay competitive in a rapidly evolving financial landscape. If this resonates with your organization, we’d love to connect.

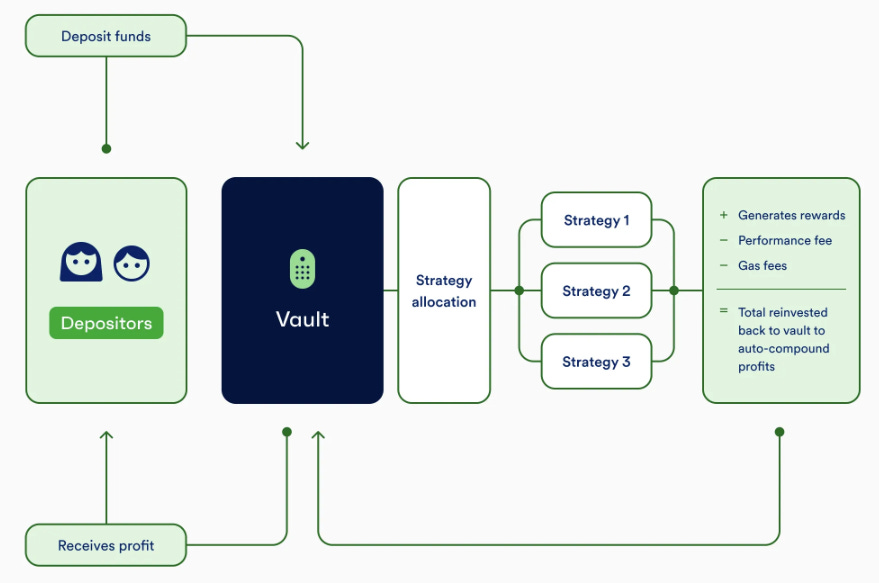

One of PayFi's most compelling innovations is how it leverages DeFi yields to create novel financial products. Consider the evolution we're witnessing: Protocols enable users to earn yields on crypto assets through staking, providing essential security to networks while generating returns. Building on this foundation, yield aggregation services automatically allocate assets across multiple DeFi protocols to optimize returns, often generating 2.5-3x more revenue per dollar than pure staking.

Some innovative applications are using crypto yields to subsidize everyday financial activities—boosting cashback rates, offsetting loan interest, or even enabling “Buy Now, Pay Never” models where yields gradually cover purchase costs. This represents a fundamental shift in how financial products can be structured. Instead of banks capturing most of the yield and passing along minimal value, PayFi systems can return more to users while still preserving margins through operational efficiency.

But this model comes with trade-offs. While the potential rewards are higher, so are the responsibilities and risks—ranging from managing custody to navigating market volatility. It’s a powerful innovation, but it won’t be the right fit for everyone.

Despite its promise, PayFi faces several significant hurdles:

Lily Liu, President of the Solana Foundation, has become a prominent advocate for PayFi. Her vision centers on equipping the world with tools to enable more efficient capital flows while expanding access to the over one billion adults globally who remain underserved by today’s economic infrastructure. At the core of this effort is programmable money. It’s the blockchain-built innovation that unlocks entirely new behaviors and product designs.

This collaborative—rather than competitive—approach may prove essential to PayFi’s long-term success. By enhancing rather than displacing existing infrastructure, PayFi brings together the trust and reach of traditional institutions with the speed, transparency, and flexibility of blockchain technology.

The most forward-thinking initiatives already reflect this philosophy. They’re not aiming to dismantle traditional finance, but to strengthen it—building hybrid systems that combine the strengths of centralized and decentralized models into something greater than the sum of their parts.

PayFi represents a practical evolution in financial technology—not a revolt. It builds on what works, delivering faster, cheaper, and programmable money movement without requiring a break from the past.

For many, the idea of self-custody and managing digital assets simply isn’t appealing—and that’s perfectly reasonable. The traditional banking model, grounded in convenience, security, and trust, still serves most people well.

But for those seeking access to blockchain-powered financial tools, the natural entry point is often their existing bank. That’s the opportunity: incumbents can integrate PayFi into familiar experiences, offering exposure without sacrificing trust. They're also best positioned to navigate evolving regulations and scale responsibly.

Innovative startups will continue to push boundaries—as they should. But the future of PayFi likely belongs to those who can bridge both worlds: combining the credibility of incumbents with the efficiency of blockchain.

At Aquanow, we help financial institutions do exactly that—bringing digital asset capabilities to trusted platforms. If the ideas above resonate, please get in touch.

Not everyone wants a new system. But everyone wants a better one. PayFi may be the quiet upgrade that gets us there.