Digital Dives

In an era marked by rapid globalization, technological advancement, and stiff competition, many industries are in flux, so events previously thought impossible or uncommon seem to happen with greater frequency.

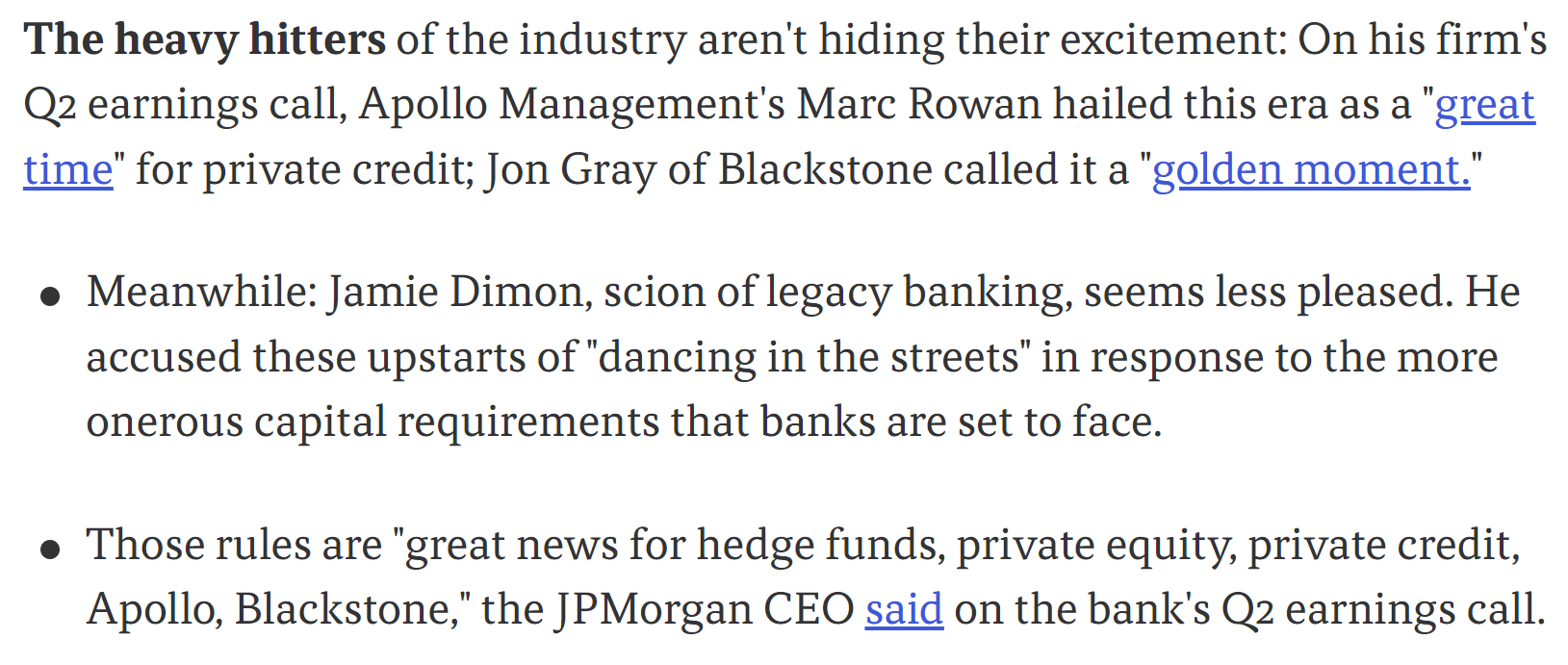

A couple weeks ago, the financial press reported a rare occurrence of a major bank executive criticizing their regulator. JP Morgan’s CEO, Jamie Dimon, made the following remarks as part of a broader, and rather colourful discourse at a recent industry conference:

To be fair, Mr. Dimon and others have been somewhat insistent about the incidence of “regulatory arbitrage” recently. Operational considerations (like assuring fair access to banking) are headwinds which aren’t as onerous or can be avoided altogether by many new competitors. Setting aside capital to protect against possible bad loans, trading/investment losses, or a sudden rush of deposit redemptions is meant to incentivize efficient practices and financial stability, but it drags on profitability.

Big Tech and other platforms have waded into lending, but more importantly, smartphones give the nimbler firms a significant advantage in processes like payments. This concerns incumbent financial institutions. So much actually, that a group of the U.S.’ largest banks are collaboratively launching a digital wallet through the jointly owned Early Warning Services. Interestingly, while the banks are electing to “team up against” the major technology platforms, they’re taking a different angle in credit. Banks have recently demonstrated a willingness to partner with outside firms to extend loans to their important corporate clients.

In recent years, the popularity of private equity (PE) investments has increased meaningfully. Institutions and high-net-worth individuals have been progressively drawn to the potential for the higher returns (and seemingly lower volatility) that private equity can offer compared to more traditional investments like stocks and bonds. Often, PE deals are structured as equity investments combined with a significant level of debt which is eventually reduced through enhanced profitability and/or asset sales. Ultimately, the goal is to enhance the equity value for an eventual monetization.

Historically, PE firms have been great friends of the banks, who used the related deal flow to generate advisory fees, trading revenue, and interest income. However, given the pace of activity and now potential for even more stringent capital rules, the landscape is starting to shift. Many buyout firms have launched private credit funds, where investors commit capital to be lent out to various borrowers, including the PE firms themselves. Here’s the JP Morgan chief again.

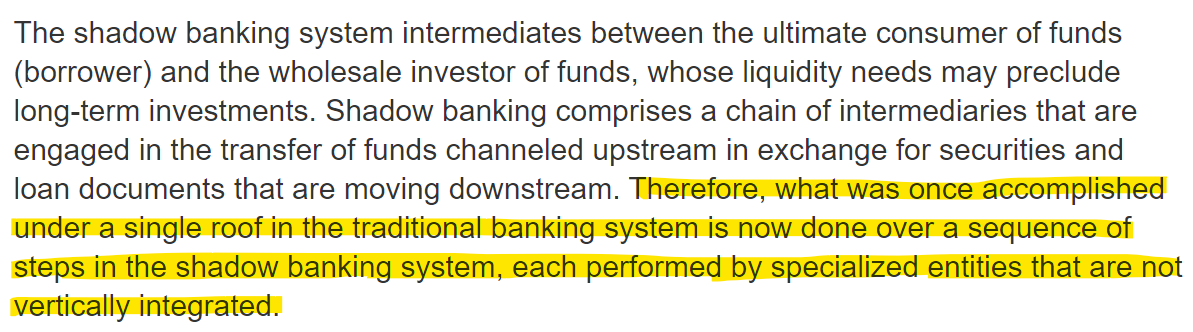

This kind of activity is sometimes called "shadow banking." Wikipedia credits Paul McCulley of PIMCO for being the first to have coined the term at the 2007 Jackson Hole Symposium. He referred to the idea as “the whole alphabet soup of levered up non-bank investment conduits, vehicles, and structures." I think of it as a group of entities that provide bank-like services such as lending, structuring, and payments but who operate with less regulatory oversight. Fintech wasn't really a thing in 2007, but I think it qualifies as a disintermediation of what banks used to do under one roof — especially if credit is extended through things like “buy now, pay later”. The term “shadow” carries an air of being untoward or illicit, but in fact, these services are integral to the world’s financial system.

Shadow banking derives some important benefits, such as greater access to credit for SMEs and others overlooked by traditional banks. Diversification tends to be a good thing. More sources of credit are likely to provide faster and more agile financial solutions. Private debt doesn’t usually come from retail savers, use additional leverage, or feature a liquidity mismatch. Smartphone payments are ubiquitous. Of course, there are risks here, too. Novel technologies can expose unpredicted attack vectors and reduced transparency could still lead to systemic contagion. After all, the current regulatory framework for the banks came into play because of the questionable practices of the broader finance industry leading up to the Great Financial Crisis.

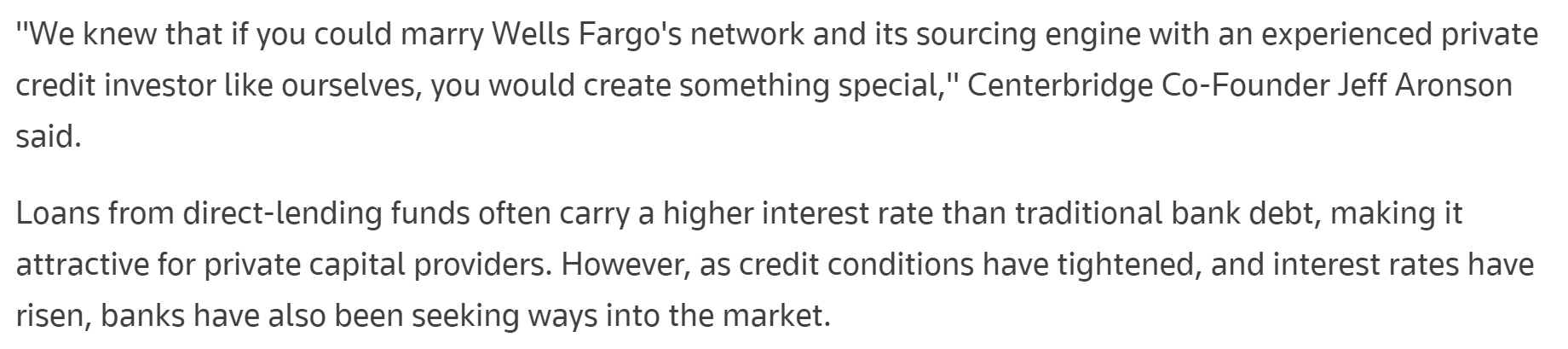

As mentioned earlier, while some executives have voiced concerns about the rise of shadow banking, several banks are taking a different approach to manage the possibility of losing wallet share to previous clients. Wells Fargo, Société Générale and other European financial institutions are teaming up with private equity giants like Brookfield and Apollo. The extent of cooperation is impressive. Certainly, some capital will be required by all parties, but by teaming up, the groups can leverage their combined scale and network with unique skills and expertise.

Last year, the Basel Committee on Banking Supervision, whose capital rules apply (at a minimum) to most of the largest banking institutions, published its finalized Prudential Treatment of Cryptoasset Exposures. There’s lots of room for interpretation, but the broad conclusion is that balance sheet requirements for digital assets will be at least as stringent as their traditional cousins and potentially prohibitively so. On top of a steep operational learning curve, this an added challenge for banks and other regulated entities to adopt the new technology. Several continue to incubate projects. However, capital is the lifeline of a financial institution, and there’s no maybe about adhering to regulation. These are the underlying forces that have driven the recent trends in lending and payments — business lines banks have led for centuries.

It appears that the finance industry is likely to take more of a “private credit” approach to crypto, by working with reputable partners to leverage each group’s respective talents and knowledge. Given banks’ increased collaboration with private equity and other financial players, it’s likely that the path forward will be multi-faceted. Those from the digital asset industry who will be successful in winning the trust of the incumbents will understand their perspectives, constraints, and objectives. Call me biased, but Aquanow fits the bill nicely and we are engaged with many.

In July of 2021, Senator Elizabeth Warren referred to those in crypto as a group of “shadowy, faceless super-coders and miners”. Unfortunately, her view on the industry hasn’t moderated, but many builders in the space wear the badge of “shadowy super coder” with pride. Personally, I think the idea of a Shadowy Super Bank sounds downright awesome and it seems like this could be the way forward.

At Aquanow, we help institutions unlock the potential of digital assets, so if you or anyone you know is considering this functionality, then please get in touch. We’d be glad to leverage our expertise to help you outperform.

If you want to contribute to the web3 movement, Aquanow is on the look for curious and motivated folks to join our team. Feel free to reach out directly or check out the current openings here.